What are the main themes?

First, protecting Australia from COVID-19, including through the vaccine rollout, tax initiatives for businesses, extending tax relief to low- and middle-income earners and giving targeted support for sectors and regions continuing to be affected by COVID-19.

Second, creating jobs, including through spending on infrastructure and skills.

Third, guaranteeing essential services through spending on areas such as aged care, mental health and NDIS.

Finally, building resilience and the security and defence capability of Australia through investing in Australia’s regions and supporting the defence industry.

Biggest winners

Indeed, businesses were among the biggest winners from tonight’s Federal Budget. There is a deep awareness within the Budget that businesses create jobs. Tax initiatives for businesses introduced in last year’s Federal Budget to encourage business spending and support the cash flow of businesses have been extended for another year to the end of 2022-23.These temporary measures are the loss carry-back provisions and full expensing and are estimated to cost $17.9 billion over four years. By helping boost cash flows and encourage businesses to spend, job creation should ensue.

The loss carry-back allows businesses to write-off any losses incurred until June 2023 against profits made on or before 2018-19 rather than on subsequent profits as usually happens. For temporary expensing, businesses with aggregate turnover of up to $5 billion will be able to write off the full cost of eligible depreciable assets of any value in the year they are first used or installed. Businesses were not the only winners.

The government is extending the low-to-middle income tax offset for another year, which delivers personal tax relief to households. This tax relief will boost demand throughout the economy. The Budget has laid a good foundation, but the path to recovery will take time.

Where does the Budget fall short?

Expectations were high that this Budget would do a lot for women. This Budget contained a package supporting the safety and economic security of women and it is a welcome step in the right direction, especially the spending on domestic violence. However, we would have liked to have seen spending measures towards helping bolster access to capital for female start-ups and scale-ups. Our research shows that access to capital is one of the biggest obstacles facing women when starting or running a business. This can be due to the lack of dedicated funding for women as well as other factors.

Another obstacle often facing women is the lack of sufficient retirement savings due to the different work patterns of women that include career breaks. Lifting female participation in the workforce helps. The additional $1.7 billion in spending on child care will help lift female workforce participation, but only modestly. More needs to be done if we are to address the lower rate of female participation and the insufficient retirement savings of women.

Deficits and Budget repair

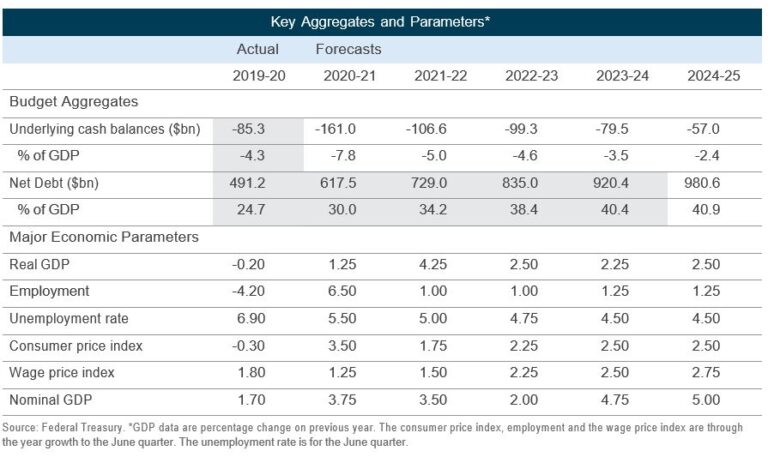

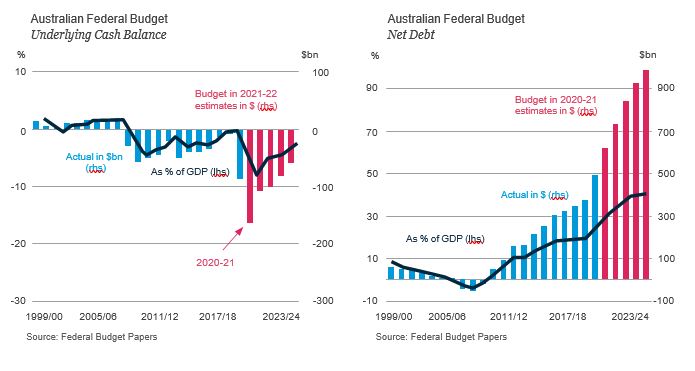

Large deficits will remain a feature over the next few years, as the focus remains on rebuilding the economy. These deficits are projected to shrink gradually. For 2022-23, a budget deficit of $99.3 billion is projected by the government and by the outer year, 2024-25, the budget deficit is expected to narrow to $57.0 billion (or 2.4% of GDP).

It is too soon to start talking about Budget repair. The economy is still in rehab and there remains considerable uncertainty around the health and economic outlook. For now, the government needs to focus on ensuring the recovery stays on the right track.

Can we afford such a large deficit?

An alternative question might be ‘can we afford not to’? The COVID-19 pandemic has been the largest hit to our economy in 90 years. Pulling back government support pre-emptively would see more people fall into unemployment and more businesses fail. Yes, the government has spent a lot and will continue to do so. This spending has been funded by increasing public debt. But we can afford it. And it is in the nation’s best interests.

Net debt will increase to 30.0% of GDP in June 2021 before hitting a record 40.9% in June 2025. While the deficit and the accompanying debt will reach a record proportion of GDP, debt in Australia relative to the size of the economy is much lower than in many other countries and is likely to remain so.

Interest rates are also at very low levels. The government can borrow money for 10 years at a miserly rate of under 2%. Such low rates make debt servicing far easier than it might have been in the past. As debt built up after the 1990s recession, net interest payments increased to 1.7% of GDP. On tonight’s figures, debt interest payments are expected to remain at 0.7% of GDP over the next few years.

When does the Budget return to surplus?

The name of the game today is rebuilding the economy, not cuts to spending and belt tightening. Those policies were tried during the depression and added to everyone’s misery. Times have changed and so has the Budget. Jobs and livelihoods come before economic dogma. Some analysts expect a surplus might be returned within the next four to five years. It’s not completely out of the question but does require a lot of cylinders to be firing all at once, including ongoing falls to unemployment, rising iron ore prices and ballooning company profits.

What about the economic outlook?

The government expects economic activity to recover to above pre-pandemic levels in the first quarter of 2021. Following the strong rebound, economic growth is expected to moderate as the economy transitions out of the initial reopening phase of the recovery. Real GDP is forecast to grow at a solid pace of 4.25% in 2021-22, before slowing to a more moderate pace of 2.5% in 2022-23. Both growth forecasts are softer than our own predictions. We expect 4.7% growth in 2021-22 and 3.0% in 2022-23.

The unemployment rate is forecast to tick down to 5.5% by June this year from the current level of 5.6%, despite earlier concerns unemployment would increase, albeit temporarily, after the conclusion of JobKeeper at the end of March. The Treasurer has emphasised his goal is to drive the unemployment rate down to below its level prior to the pandemic, which was around 5.0%. The government forecasts the unemployment rate to fall below 5.0% in 2022-23 and reach 4.50% in 2023-24, which is a rate Federal Treasury has estimated to be the rate consistent with full employment in the economy. The Reserve Bank expects 4.5% to be reached sooner, as do we.

The government has forecast that wages will pick up from their current lows, although the numbers still aren’t great. The forecasts show wages growth hitting 2.75% by June 2025. The RBA wants to see wages growth over 3% to get inflation back in its target band.

The iron ore price is forecast to decline to US$55/tonne by the March quarter of 2022. The iron ore price has soared over the recent period, due to strong Chinese demand and supply disruptions in Brazil and is currently sitting over US$200/tonne. We expect the iron ore price will remain much higher than the government’s forecast.

The government’s conservative growth and iron ore forecasts means there is a good chance the government’s bottom line will turn out better than forecast in this Budget.

Net overseas migration has been smashed by international travel restrictions. It is forecast to fall from 194,000 persons in 2019-20 to around -97,000 by the end of 2020-21. Only a slight improvement to -77,000 is predicted for 2021-22. A recovery to 235,000 persons is anticipated in 2024-25.

The RBA is holding the cash rate at a record low of 0.1%, targeting the 3-year government bond yield and is purchasing longer dated bonds under its quantitative easing program. Tonight’s Budget has not changed our view of RBA policy. We do not expect the cash rate will be lifted until 2024 at the earliest.