Schedule a Chat

Contact Info

Suite 17.03, Level 17

20 Bond Street

Sydney NSW 2000

INSIGHTS WITH EVALESCO

TOPICS DISCUSSED

Decades of peace in Europe were shattered on February 24th, 2022 when Russia invaded Ukraine. We extend our thoughts and sympathy to everyone affected and our hearts go out to all those suffering. What is reassuring is the amount of support throughout the world in standing with Ukraine.

Without trying to diminish the human effects of the invasion, readers of this letter will no doubt be concerned about the effect on their investments. To comprehend the gravity of the situation, we’ve broken it down into four sections: overview, global reactions, the Russian economy, and global markets.

Overview

The roots of the conflict are best understood by looking at the geography. Ukraine sits with Russia to its east, and Poland, Romania, Slovakia and Hungary to the west. All of those countries to the west are NATO members. Since Ukraine gained independence in 1991, Russia has long resisted Ukraine’s move towards the European Union and western democracies. More recently in 2014, Putin’s soldiers infiltrated Crimea, annexing the peninsula from the rest of Ukraine, effectively turning it into a Russian state despite going against international law.

Global Reactions

An array of sanctions were placed against Russia following the invasion. The intensity of the sanctions increased through March in a coordinated effort around the world. The most significant of these being the financial measures taken, and the sanctions on oil and gas. Examples of significant government sanctions are below:

Peace negotiations between Ukraine and Russia are ongoing at the time of writing. Even if an agreement is reached, Europe has realised just how reliant they are on Russia for oil and gas. Europe need to decide what reductions need to be made moving forward, and where energy could be sourced from otherwise. If nothing comes of the negotiations and further military action is the result, what does the West do? Further sanctions could be devastating for Europe given a quarter of its oil and about 40% of its gas comes from Russia.

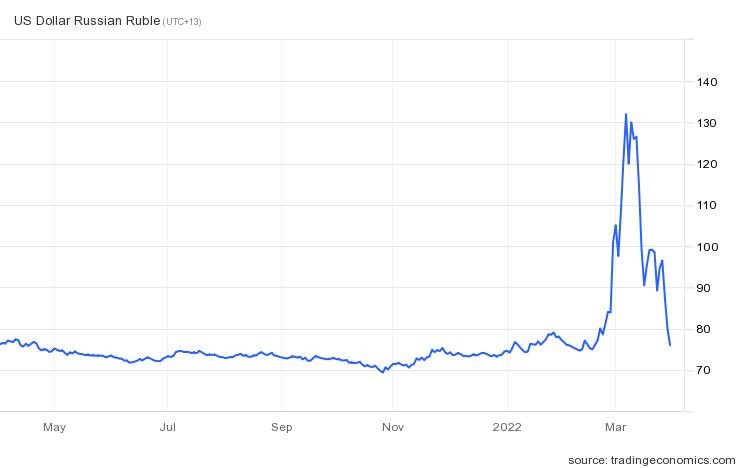

Figure 1: Russian Ruble vs USD.

Russian Economy

Russian Economy

Russian economic policymakers went to extraordinary lengths to help maintain financial stability since the invasion. Three key aspects required for macroeconomic stability see Russia in a very uncomfortable position: the exchange rate, monetary policy and capital flows.

The ruble depreciated swiftly from around 80 rubles per USD, to 130 rubles per USD. By the end of March the ruble stabilised somewhat (Figure 1) following decisions to limit the flow of capital outflows and increase the key interest rate in Russia. The central bank took the decision to raise the key interest rate from 9.5% to 20% (Figure 2). Restrictive measures regarding capital flows included orders for Russian exporters to sell 80% of their foreign currency reserves and banning Russians from foreign currency sales for six months. The Russian government also prohibited foreign investors from moving investments out of the country, barred companies from paying dividends to shareholders overseas, and constrained payments to outside investors holding ruble-denominated debt.

The Russia stock exchange was closed on February 25th, but not before a 50% fall in the MOEX Russia index (top 50 stocks). However, the iShares MSCI Russia ETF was still able to be traded on the NYSE. This ETF was down over 80% year-to-date by the end of March!

Figure 2: Central Bank of Russia key interest rate

Global Markets

Global Markets

The invasion caused a direct shock to commodity markets. Most notable was the shock to oil and gas markets. The price of Brent crude increased to over USD130 a barrel, whilst WTI reached over USD120. Oil prices were down around USD102-USD108 by quarter-end, in part due to the US announcing that one million barrels of oil per day would be released from its Strategic Petroleum Reserves for a period of six months starting in May. In gas markets, EU natural gas futures spiked at €345 per megawatt-hour intraday on March 7th. A note by JPM estimated that if Russia were to stop supplying gas to Europe, the price of gas would need to average €200/MWh for 2022 to create the amount of demand destruction required to match the loss of Russian gas supply to Europe for the rest of 2022. The quarter-end price was approximately €120/MWh.

Headline equity markets in Europe reached their lowest point in early March with falls of 7%-19% compared to the start of the year. By 31 March these stabilised, with the FTSE 100 even posting a slightly positive return for the quarter, though the DAX was still down 10%. US markets were down 9%-20% at the lowest point, before finishing down 5%-10% by 31 March. The ASX200 performed considerably better through the quarter given the rise in commodity prices, with a positive return of 0.7%.

Bond yields rose considerably through the quarter. Whilst COVID-related disruptions to supply chains worked their way into inflation figures through 2021, the latest expectations of inflation have been exacerbated by the devastating invasion of Ukraine and the consequent disorder to commodity markets. Over the past year the market has moved from expecting ‘transitory’ inflation, to firm expectations of more sustained inflation.

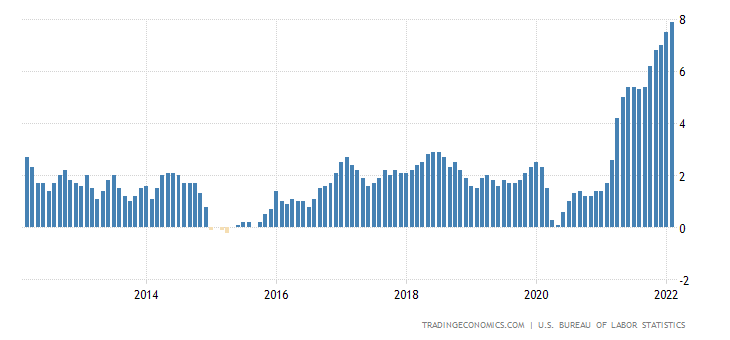

Figure 3: US Headline Annual Inflation

Inflation in the US hit 7.9% in February (Figure 3), the major contributor being energy. This is the highest level since January 1982. Even taking out the effect of energy and food, the CPI figure rose to 6.4% which is the highest in 40 years.

Inflation in the US hit 7.9% in February (Figure 3), the major contributor being energy. This is the highest level since January 1982. Even taking out the effect of energy and food, the CPI figure rose to 6.4% which is the highest in 40 years.

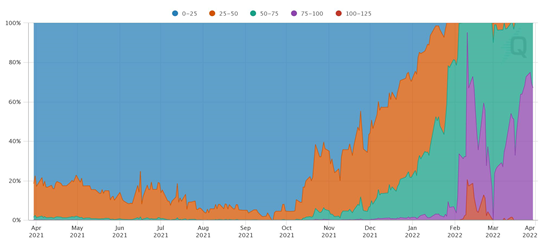

Figure 4 shows the market pricing towards the end of March for the Fed Funds rate decision on 4th May. The purple area shows what chance the market thinks the Fed will move the rate to 0.75%-1.00% by the 4th May meeting (currently it is 0.25%-0.50%). At the end of March, the market was pricing about a 70% chance. The green area shows the probability the target rate will move to 0.50%-0.75%, so about a 30% chance as at the end of March. Keep in mind that the target rate probabilities are constantly changing. To give the 70% probability more perspective, the market was pricing a probability of just 16% a month earlier.

Figure 4: Target Rate Probability History for Federal Reserve Meeting on 4 May 2022

Expectations of a higher Fed rate pushed up the shorter end of the US yield curve. Yields at the longer end of the curve also increased, though a more pessimistic economic outlook started to weigh on those longer yields. The net result through the quarter was a broadly flatter yield curve, the US 10Y/2Y gap was down from 86bps to 3bps by the end of March. Parts of the curve actually ended the quarter inverted with the 3Y (2.51%) and 5Y (2.46%) yields higher than the 10Y yield (2.36%).

Expectations of a higher Fed rate pushed up the shorter end of the US yield curve. Yields at the longer end of the curve also increased, though a more pessimistic economic outlook started to weigh on those longer yields. The net result through the quarter was a broadly flatter yield curve, the US 10Y/2Y gap was down from 86bps to 3bps by the end of March. Parts of the curve actually ended the quarter inverted with the 3Y (2.51%) and 5Y (2.46%) yields higher than the 10Y yield (2.36%).

In Europe, investors are pricing a greater chance of higher ECB policy rates following on from the US. However, the ECB indicated in mid-March that “any adjustments to the key ECB interest rates will take place some time after the end of the Governing Council’s net purchases under the APP and will be gradual.” The deposit facility rate has been -0.5% for the past eight years, but the market is now pricing in 50bps of hikes by year-end to bring it back to zero. Yields increased through the quarter, notably the German 2-year bund broke through into positive territory briefly for the first time since 2014, whilst the 10Y bund was positive for the first time since January 2019 (55 bps by quarter-end).

Back down under, Australian GDP figures showed a bounce of 3.4% for the December quarter, following a contraction of 1.9% during the September quarter. The bounce came as NSW, Victoria and ACT surfaced from extended lockdowns. This compares to a pre-COVD growth rate of 0.4% in the December 2019 quarter. The annual rate increased slightly from 3.9% to 4.2% to the end of December 2022.

The RBA kept the cash target 0.10% at the March meeting as inflation increased to 3.5% to the end of December. Whilst inflation is rising, the RBA sighted uncertainties around the persistence of the rise in inflation due to global energy markets and supply-side problems.

Outlook

Going forward, global growth will be lower than was forecast before the invasion. Europe will be the hardest hit. Inflation will continue to rise in the near term. Major uncertainties arise from the impact of energy markets on inflation/growth, but also how quickly supply chains can get back to some sort of normal.

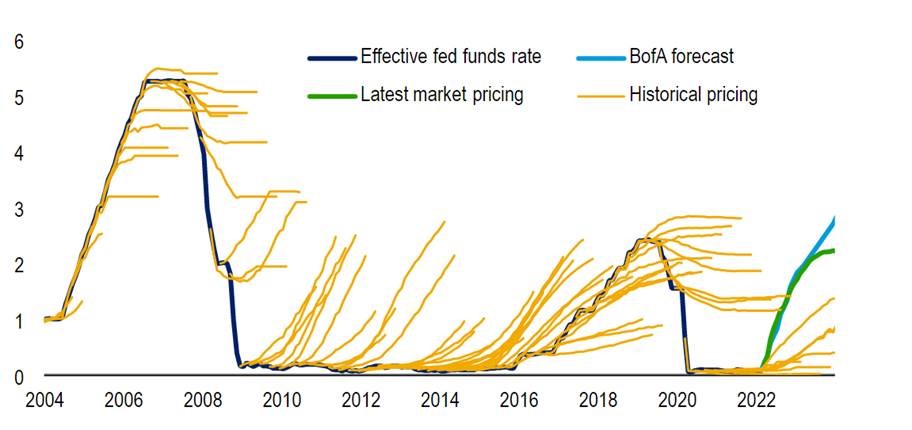

A major risk confronting the global economy and markets is a policy mistake from central banks. The RBA is one of the more dovish central banks at this time. Conversely, the US Fed are much more hawkish. How that hawkishness flows through to actual increases in the Fed funds rate remains the major quandary. Figure 5 shows just how hawkish markets have been in the past (yellow lines), whilst more often than not the actual Fed fund rate stayed lower for longer. Gradual hikes may not contain inflation, but more hikes may result in a harder landing than desired.

Figure 5: Historical Market Estimates for the US Federal Reserve Funds Rate. Source: Bank of America; Franklin Templeton

You can download the entire Quarterly Investment Update HERE

Regards,

Marshall Brentnall, and the AAN Investment Committee

SHARE OUR INSIGHTS

Share on Facebook

Share on Email

Share on Linkedin

NEWSLETTER

Evalesco Financial Services Level 17, 20 Bond Street Sydney NSW 2000

Phone: (02) 9232 6800

The information provided on and made available through this website does not constitute financial product advice. The information is of a general nature only and does not take into account your individual objectives, financial situation or needs. It should not be used, relied upon, or treated as a substitute for specific professional advice. We recommend that you obtain your own independent professional advice before making any decision in relation to your particular requirements or circumstances. Evalesco Financial Services do not warrant the accuracy, completeness or currency of the information provided on and made available through this website. Past performance of any product discussed on this website is not indicative of future performance. Copyright © 2019 Evalesco Financial Services. All rights reserved